SPAC. This 4-word acronym, if you’ve followed news related to tech or investing recently, have come up a hell of a lot more often.

I spent over 9000 hours on MS Paint to make this OC meme, please clap.

As in the last edition, so many smarter people have talked about SPAC. I’ll have them explain what SPAC is.

A SPAC (“Special Purpose Acquisition Company”, or “blank check company”), [Chamath] told us, was a new way we were going to help take big tech companies public. Going public is an important moment in a company’s life. … The current way we do it - the IPO (Initial Public Offering) - stinks. (danco)

In layperson’s terms, this means a shell company1 is formed, raises money from investors, IPOs immediately after, finds a late-stage private company, then merges with them so that the late-stage private company is now public. (luttig)

SPACs = Schrodinger’s stock?

Using one of my favorite ways to explain (analogies!), when you buy the IPO of an established company, it’s like buying a new camera box with all the original stuff in it. When you buy a SPAC, it’s like buying only a box with nothing inside, then the seller promises you that he’ll find a suitable camera that you’d definitely love in a set amount of time, but if he fails to do so, you can get your money back.

Is it going to be a DSLR? A mirrorless? A Leica? Or a Nokia 7650? No one knows!

That basically means buying a SPAC is a bit like buying into a Schrodinger’s cat situation2, except it’s a company rather than a cat, and instead of Schrodinger, it’s some guy who promotes the empty box. This guy is called a SPAC sponsor.

Chamath, a former high-flying FB exec, started the recent tech craze for SPACs in late 2019 when he became a SPAC sponsor and took Virgin Galactic3 public through SPAC.

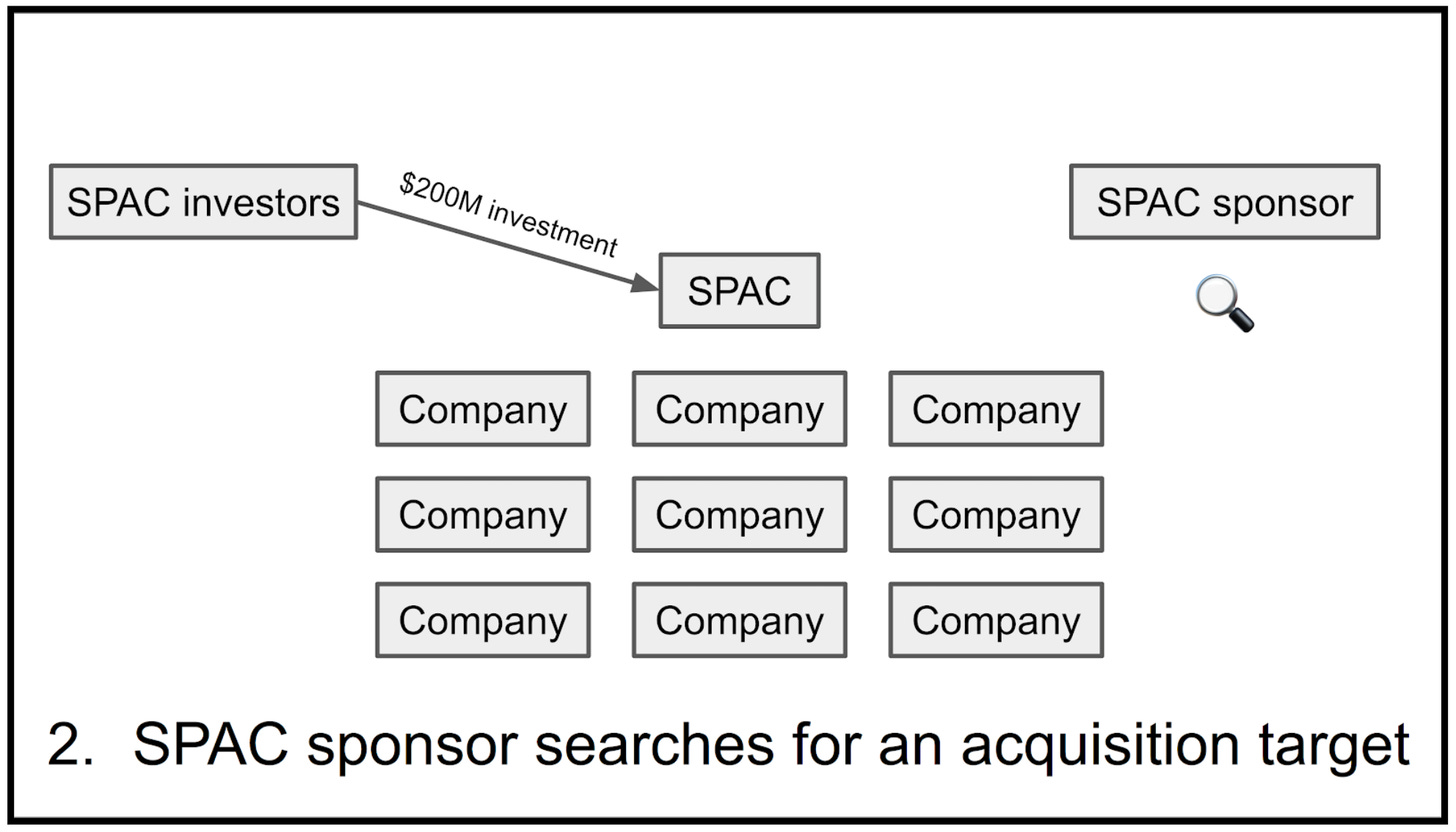

So why is everyone dying to be a sponsor and kickoff their own SPAC? To answer this, we may need to first understand how SPAC works. This might get a bit technical, and I’m doing my best to try and simplify it, but I’m failing pretty hard.

Scroll to the next section for a quick tl;dr summary and to jump into discussion.

1. Kicking off the SPAC party

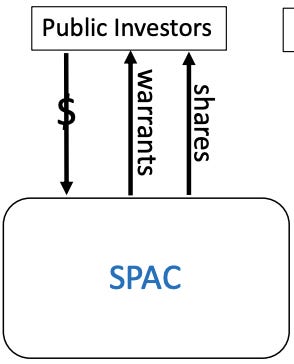

A SPAC sponsor creates a shell company, raises funds from investors, and goes IPO in just a few months.

SPAC investors and sponsors get BOTH shares and warrants4 of the shell company, which are all tradable on the market.

The SPAC sponsor promises the SPAC investors that they’ll merge with an awesome company usually in 24 months, accounting for a 4-6 months merger time. This means the sponsor has around 18 months to quickly find a suitable company.

Meanwhile, the investors’ money is kept in a trust that can only invest in safe, short-term US government bonds, up until the merger is completed or 24 months is up. The funds can only be used to:

Investors can redeem shares before a merger is concluded

Note: founder shares can’t redeem shares

3. Target confirmed, lock and load!

4. 3… 2… 1… Houston, should we lift-off…?

Once the due diligence are all taken care of, next comes the most important thing: the sponsor goes to the SPAC shareholders and ask for approval to merge (or “de-SPAC”).

If they reject, the sponsor has to find a new target company before the time is up. When the time is up, then all the investors’ money is returned, and the founders’ shares as well as all warrants are worth nothing.

If they accept, an announcement of the intent to merge is made, and SPAC investors have the option to:

Keep holding the shares and warrants, or

Redeem the shares for the original amount + interest, AND keep the warrants

Therefore, the SPAC investors’ money is essentially risk-free: they get at least the original amount back if the SPAC didn’t work out. If the SPAC was a hit, they can sell the shares at a gain, or redeem it for the original investment amount. They still also get to keep the warrants, which means that even if they redeemed, they still have a potential upside through the warrant.

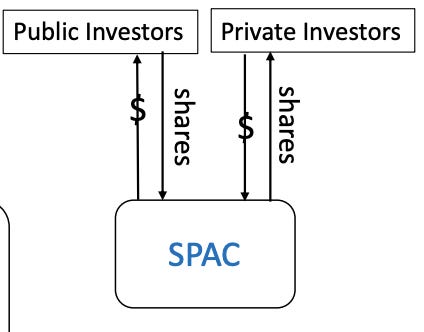

5. PIPE and it’s done!

The median SPAC redemption is around 73% of the initial capital, which means if you raise a $200M SPAC, and successfully find a merger target, around $150M will be redeemed, leaving you with around $50M to execute the merger successfully.

For SPAC investors (dominated by hedge funds): it’s an easy way to park your money for 2 years (essentially risk-free) while getting potentially unlimited upside from the additional warrants received.

For SPAC sponsors: it’s a very lucrative structure that lets you get 20% of a company for really cheap, potentially gaining capital gain and more fees from the ensuing PIPE transactions, giving you a median return of 200%.

Companies: to SPAC or not to SPAC?

For target companies, SPAC is only one way out of many to go public.

Then, why SPAC instead of the other routes?

The certainty of going public.

When you sign the merger agreement, you know you’re going public, and you know the price. You negotiate with one person—the sponsor of the SPAC—and you agree on the price, and then you sign the agreement and the deal is pretty much locked in. You don’t necessarily know how much money you’re raising—how many shares you'll sell—because the investors in the SPAC have the right to ask for their money back if they don’t like the deal. But you’ll at least raise some money, at a fixed price. (Matt Levine)

The speed of going public.

The SPAC is much faster than an IPO or a Direct Listing, which will both take 6-7 months from beginning to end. With a SPAC you could be public in two-months from when you start the process (assuming you have your house in order). (Bill Gurley)

On the flip side, why not SPAC?

The uncertainty of everything else besides confirmation of going public:

When you sign the merger agreement, you know you’re going public, and you know the price. You negotiate with one person—the sponsor of the SPAC—and you agree on the price, and then you sign the agreement and the deal is pretty much locked in. You don’t necessarily know how much money you’re raising—how many shares you'll sell—because the investors in the SPAC have the right to ask for their money back if they don’t like the deal. But you’ll at least raise some money, at a fixed price. (Matt Levine)

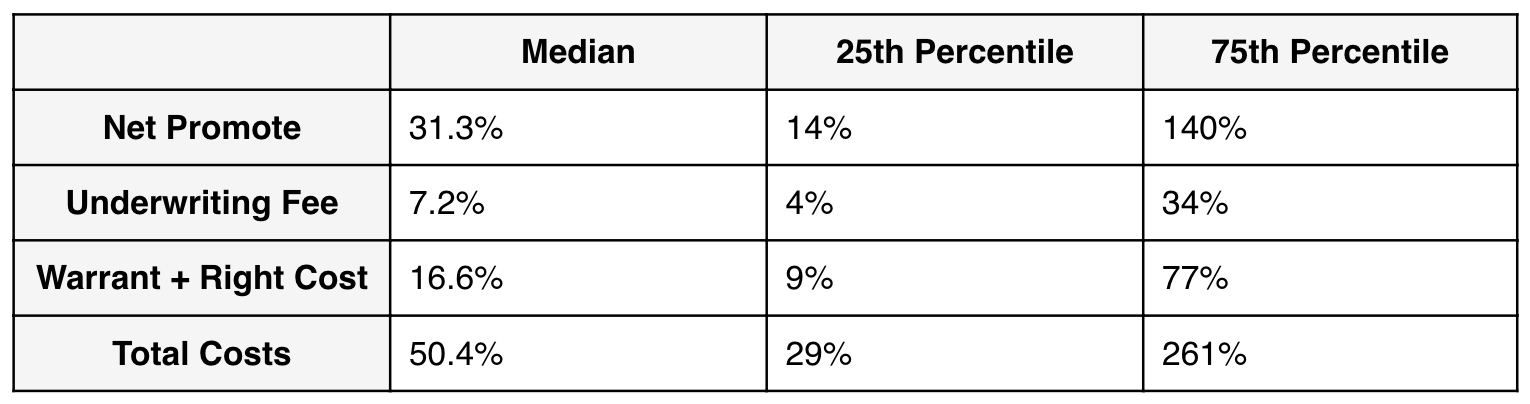

Total IPO costs, including the pop, are roughly 20% to 22% of cash raised in in an IPO. … The median SPAC’s dilution amounts to a staggering 50.4% of cash delivered in a merger.

But then again, IPOs also have their own long history, with a 1922 book titled “Successful Stock Speculation” giving advice on buying IPOs: Don’t.

So who knows, SPACs are still evolving, it may be early days yet for the instrument, and this might be another case where we see a financial innovation beating out many regulators’ slow attempt to provide liquidity to startups in India, Indonesia, and others.

This is a really long post, with lots of details sprinkled in-between that leaves me not a lot of time to put jokes in… but that really says how complex SPAC is, especially for people without any background in finance, and I don’t think I explained it simple enough.

Anyway, that’s it for today but feel free to ping me anywhere you know I might be to ask any questions so that I can explain further, or to correct me on the above so I can go on and fix it.

Shell companies are registered, legal companies with no operations. Like you registering a new Instagram account without posting anything on it. At least you can use it for other things you won’t do with your normal account, like stalking people’s public feeds or stories.

Virgin Galactic builds spaceships that took Tom Hanks, Brad Pitt & Angelina Jolie, Michael Schumacher, Stephen Hawking, and other tourists to space. Yes, even Paris Hilton went to space.

Receiving warrants is like receiving the privilege to buy something at a fixed price (“strike price”), no matter what the current price is. For example, if someone gave you a warrant for the rarest Pokemon cards with a $100 strike price, you can buy it for $100 anytime until the warrant expires.

Since the SPAC is already a public company, this essentially means that the SPAC issues new shares to private investors (not to the public). It’s like selling your lockdown sourdough bread only to your friends instead of using FB Marketplace or Craigslist.